Till now, we have discussed the basic concepts in finance. Suppose you have not seen those posts. You can check them out here. In this post, we are going to discuss something which is not very often discussed in the world of finance.

Let’s start by understanding what a loan is and what a credit line is.

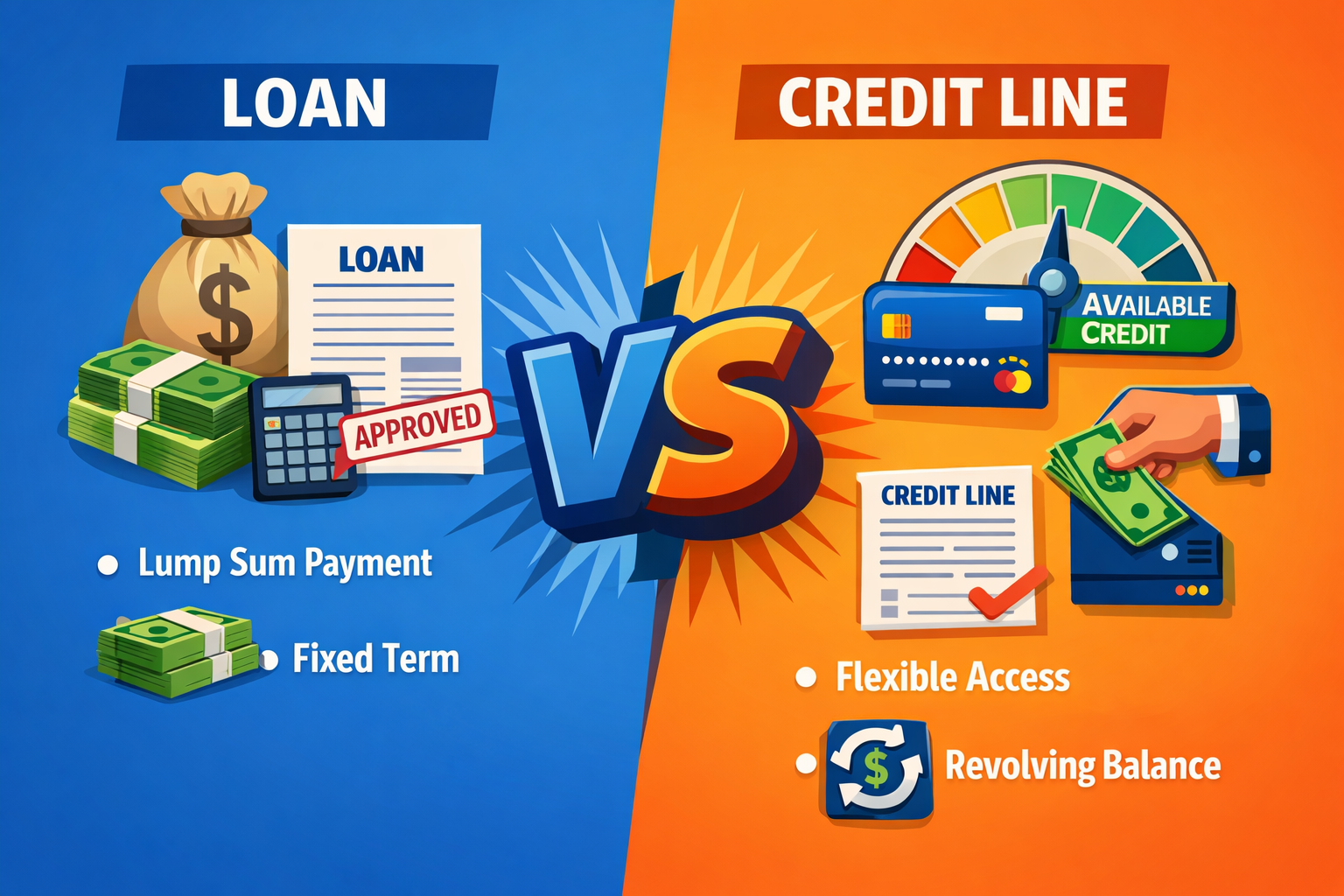

Quick Answer: A loan is a fixed lump sum borrowed upfront with scheduled repayments, while a credit line is a flexible borrowing arrangement where you can draw funds up to a limit, repay, and reuse as needed.

When individuals or businesses seek financing, two common options are loans and lines of credit. While both provide access to funds, they differ significantly in structure, flexibility, and use cases. Understanding these differences helps borrowers choose the right tool for their financial needs.

What is a Loan?

A loan is a one-time, fixed lump sum borrowed from a lender. borrowers repay in regular instalments ( monthly, quarterly) depending on the plan over a fixed term. The interest is charged on the entire loan amount from the start. This is best for specific, large expenses such as buying a home, car, or funding a project. In this the payments are fixed, making budgeting easier.

What is a Line of Credit?

A line of credit is a flexible borrowing facility with a maximum limit. You can draw funds as needed, repay, and reuse within the limit. Interest is charged only on the amount actually used, not on the full limit. It is ideal for ongoing or unpredictable expenses, such as working capital, emergency costs, or seasonal business needs. Functions like a credit card but often with lower interest rates.

Key Differences between a Loan and a Line of Credit

| Feature | Loan | Line of Credit |

|---|---|---|

| Amount | Fixed lump sum upfront | Flexible, up to a pre-set limit |

| Usage | Single purpose (home, car, project) | Multiple/ongoing needs |

| Withdrawals | All at once | As needed, repay and reuse |

| Interest | Planned large expenses | Flexible, often with minimum payments |

| Repayment | Fixed schedule | Flexible, often minimum payments |

| Best For | Only on the amount used | Short-term, variable cash needs |

Practical Example

Suppose you borrow INR 10 lakh to buy a car. You will receive the full amount upfront and repay it in fixed EMIs over a fixed tenure. This is a loan. Whereas if you have an INR 10 lakh credit line, you withdraw INR 2 lakh for renovations, repay it, then later withdraw 3 lakh for a medical emergency. The interest applies only to the withdrawn amount

Choosing Between Them

Pick a loan if you have a specific, one-time expense and want a predictable repayment. Choose a line of credit if you need ongoing flexibility and want to pay interest only on what you use.

In summary, Loans provide stability and structure, while credit lines offer flexibility and adaptability. The right choice depends on whether your financial need is fixed and planned or variable and recurring.

This is all for this post, hope you got to learn something new. Don’t forget to follow my Facebook and Instagram pages for regular updates. See you all in the next post. Till then keep learning.