Till now we have understood how the rich get richer by accumulating assets instead of liabilities. if you have not read that post you can check it out here.

But what type of assets? And how do they select which assets to keep in their portfolio?

In this post, we are going to discuss the secret or not-so-secret force that helps the rich to get richer and maintain their wealth. For understanding this secret we need to understand two simple terms.

Simple Interest vs Compound Interest

So we are going to refresh some of our elementary school mathematics here. The concepts of simple interest and compound interest are not new to anyone who has gone through elementary school, but majority of the people would not have understood how important these are in real life.

Simple Interest

So to refresh our memory Simple interest is a form of return in which the interest is calculated on the initial principal amount. So for example, we have put 100 units to work and are promised a simple interest of 8% per year for 5 years.

The total interest that we will be getting at the end of the five years would be 40 units. This simple interest is calculated according to the following formula:

Simple Interest = Principal Interest x Interest rate x duration

Compound Interest

Whereas in the case of compound interest, this would be very different because in this the interest is not calculated on the initial or original principal amount but on the current principal amount.

So taking the same example as the previous one with putting 100 units to work at an 8% annual interest rate for 5 years we will have end up with a total interest of 46.93 at the end of 5 years. Compound interest is calculated using the following formula:

Compound Interest = Principal x [ (1+ Interest rate)duration – 1]

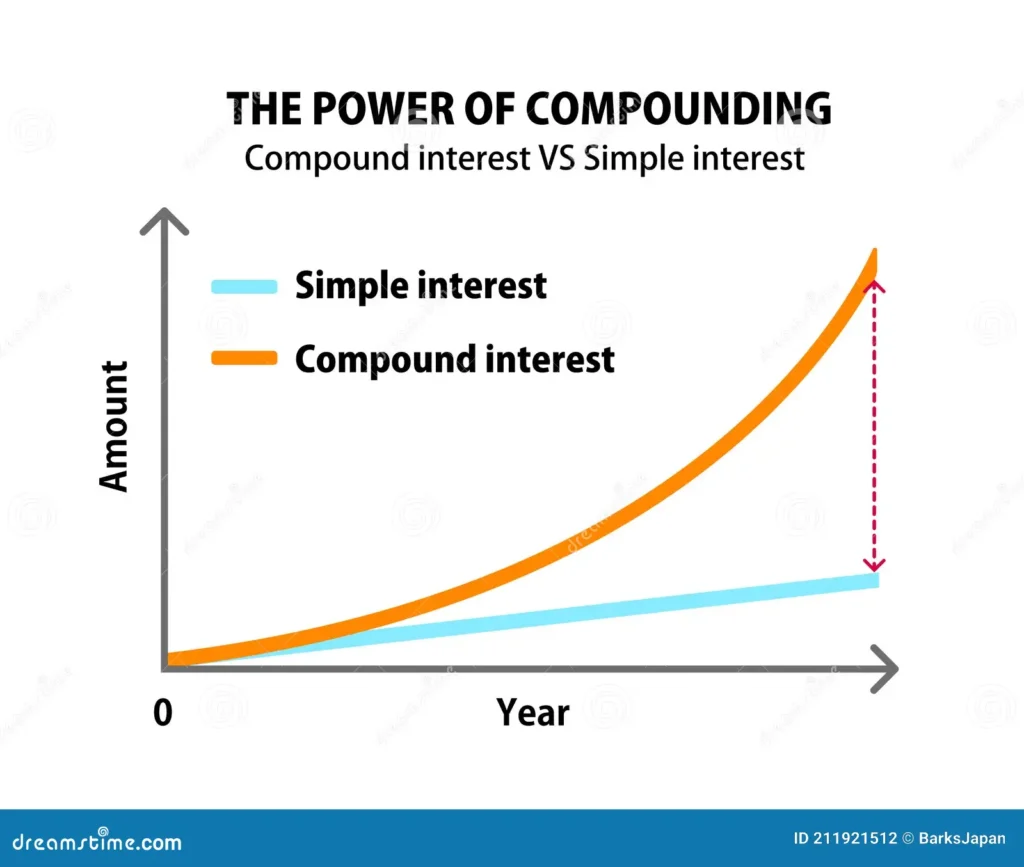

Pic credit – dreamstime.com

The above image shows the variation in returns with time for simple interest and compound interest. The blue line is the simple interest and the orange curve is compound interest. As you can see the returns of compound interest start to diverge from the simple interest by a good margin for the better as duration increases.

So now the question arises when we have the same interest and for the same duration how are the results so different?

The answer to this lies in the nature of how the interest is earned in simple interest the interest is only calculated on the initial value provided, whereas in compound interest the interest is calculated on the incrementing value of the principal amount year on year. Thus as the duration increases the interest earned increases and it might very well happen that with a suitable duration, the interest earned on a certain year might very well cross the initial principal amount.

Application of Compounding

Till now we have understood the difference between simple interest and compound interest. Now what is the use of this compounding effect? Compounding is a very integral part of everyone’s life, not only from a return point of view but from a general life perspective. To put things in perspective if you have ever tried to do anything new or learn anything new the progress might have seemed very slow initially but after a certain amount of devoted time, it becomes easy to do or learn that thing.

So when we say the rich accumulate assets, we mean they accumulate riches which exhibit a compounding effect or tend to exhibit a compounding effect that helps them increase their worth.

Exponential Returns

So how do the rich manage to grow their wealth exponentially? If you analyze the formula of compound interest there are three components to it, Interest, Principal amount, and duration (time). Let’s understand and analyze the role of all three to better understand their role in an exponential increase in wealth.

Interest vs Return

In simple words it is the compensation paid to a lender for the lending of the capital. Returns are analogous to interest except for one thing interests are generally guaranteed whereas returns are not.

For example, you can deposit a certain amount in your bank savings account and get a certain amount of guaranteed interest on the deposited amount, whereas you can’t say with certainty if you will get the same return from stock as it has given in the past, it might very well underperform or overperform. This is the risk associated with equities and this is what separates the concept of return from interest.

Duration (time)

Duration or period plays an important role in the return generated on your investments. The longer you are invested the higher amount you can generate as compared to someone who is invested for a shorter duration given that both generate same return every year.

In equities, it is said that if you invest in an index for a long duration the risk of losing money almost goes to zero. Therefore a person invested in the index for a longer duration .

Now there are other nuances to it that it’s hard for two people to generate the same return, etc but we will leave that here. So as a general thumb, the risk of negative returns decreases and the chances of making a good return increases when the duration is longer as compared to shorter.

Principal Amount

The principal amount is analogous to the investment amount in the compounding equation. In terms of returns, our returns depend a fair bit on the initial investment amount.

For example, if we generate a 10% return on 1000 it is 100, whereas if we generate a 10% return on 1000,000 it’s 100,000. So what has changed here? The answer here is the principal amount or the corpus. So the larger the principal larger the return. A note of caution that the opposite is also true, that is -10% of 1000 is -100, whereas -10% of 1000,000 is 100,000.

Therefore if the returns are very predictable then we can put a larger corpus upfront to generate a larger return on our investment.

Magic of minimal interest difference

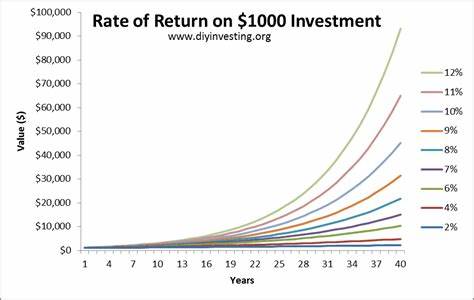

Till now we have seen the impact of all three variables on return. But there is one more nuance of return that might surprise you. Observe the image below.

Pic credit – diyinvesting.org

What did you understand from the image? If you observe that difference in returns over a 40 year period between 11% and 12% it’s large, between 10% and 12% percent it’s even larger, and so on. Therefore even a variation of 1% return produces a huge difference in return over a long duration.

All this said compounding also has a dark side. If you continue to generate negative returns it will eventually erode your corpus or principal over the same period.

So to summarize everything the compounding effect is a very helpful force if it works in your favor. A person has to evaluate all three variables that is return, corpus, and duration for making an investment decision. A person should know how long is he/she willing to deploy his money/capital, how much capital is he/she willing to deploy, and what is return he/she is expecting against the risk he is taking.

So this is all for this post. Don’t forget to follow my Facebook and Instagram pages for regular updates. See you all in the next video till then keep learning.