Till now we have discussed assets and asset classes. If you have not read about them you can read it here.

Owning assets is good. But are you willing to pay any price to buy that asset? If not then how do you determine the price of the asset at which you are willing to buy the asset, that is how do you determine what is the right price for that asset? Since everything comes with a cost, knowing the right cost is crucial for generating good returns. In this post, we will understand how to value different assets and asset classes.

First of all, let’s start by understanding what valuation means.

Valuation

Valuation in simple words is the process of determining the present worth of an asset or a company. It involves assessing various factors to estimate how much something is worth in monetary terms. This can apply to a wide range of things, including stocks, real estate, businesses, precious metals, and more. It is an analytical process. It provides a foundation for understanding the true worth of assets and making rational choices based on that understanding.

The methods and approaches used in valuation can vary depending on the type of asset being valued, but the goal is generally to arrive at an estimate of what a willing buyer would pay a willing seller in an open and competitive market. In general economics, the value of an instrument is said to depend on the supply and demand of that instrument in the market. But apart from these, there are some commonly followed approaches to value the different asset classes which we will discuss in this post.

Importance of Valuation

We understood that valuation is the process of determining the worth or value of an asset, company, or anything else that has monetary value. But what is the use of these valuations in the real world? Valuations are crucial for the reasons given below:

- Investment Decisions: Investors rely on valuation to decide which assets or companies are worth investing in. It helps them assess whether an asset is undervalued or overvalued, that is whether it is the right time to buy them or not.

- Financial Reporting: Accurate valuations are necessary for financial reporting and accounting purposes. They ensure that a company’s financial statements reflect the true value of its assets and liabilities.

- Mergers and Acquisitions: In the case of mergers and acquisitions, valuation is essential to determine the fair price for the companies involved. It helps negotiate the terms of the deal.

- Financing: Companies often need to obtain financing from banks or investors. Accurate valuation helps lenders and investors understand the company’s worth and its ability to repay loans or provide returns.

- Taxation: Governments use valuations to determine tax liabilities. For example, property taxes are based on the assessed value of the property.

- Litigation: Valuations are often used in legal disputes, such as divorce settlements or shareholder lawsuits, to determine the value of assets involved.

- Strategic Planning: Companies use valuations to make informed decisions about expansion, divestment, or restructuring. It helps them understand the value of different parts of their business.

- Performance Measurement: Valuation metrics are used to measure the performance of companies or investments over time, helping stakeholders make better decisions.

Understanding valuation is fundamental in various fields, from finance and real estate to economics and law. It forms the basis of making informed and rational decisions.

Equity valuation

Valuing equities involves several methods, each providing a different perspective on the potential worth of a company’s stock. Here are some common methods:

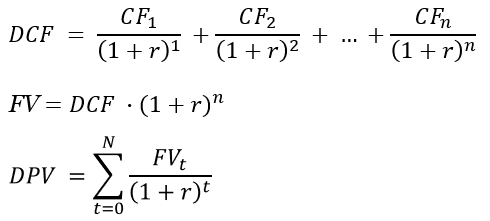

- Discounted Cash Flow (DCF): This method calculates the present value of expected future cash flows. It involves forecasting the company’s future cash flows and discounting them back to their present value using a discount rate. The sum of these present values is the intrinsic value of the equity.

- Forecasting Cash Flows: Project the company’s free cash flows (FCF) over a specific period (usually 5-10 years).

- Terminal Value: Estimate the value of the company beyond the forecast period using methods like the perpetuity growth model or exit multiple methods.

- Discount Rate: Determine the appropriate discount rate, often the company’s weighted average cost of capital (WACC).

- Calculate Present Value: Discount the projected cash flows and terminal value back to their present values and sum them up to get the intrinsic value.

2. Price-to-Earnings (P/E) Ratio: This is a popular valuation metric that compares a company’s current share price to its earnings per share (EPS). A high P/E ratio may indicate that the stock is overvalued, while a low P/E ratio may suggest it is undervalued.

- P/E Ratio: Calculated by dividing the current market price per share by the earnings per share (EPS).

- Benchmarking: Compare the P/E ratio with industry peers or historical averages to assess relative valuation.

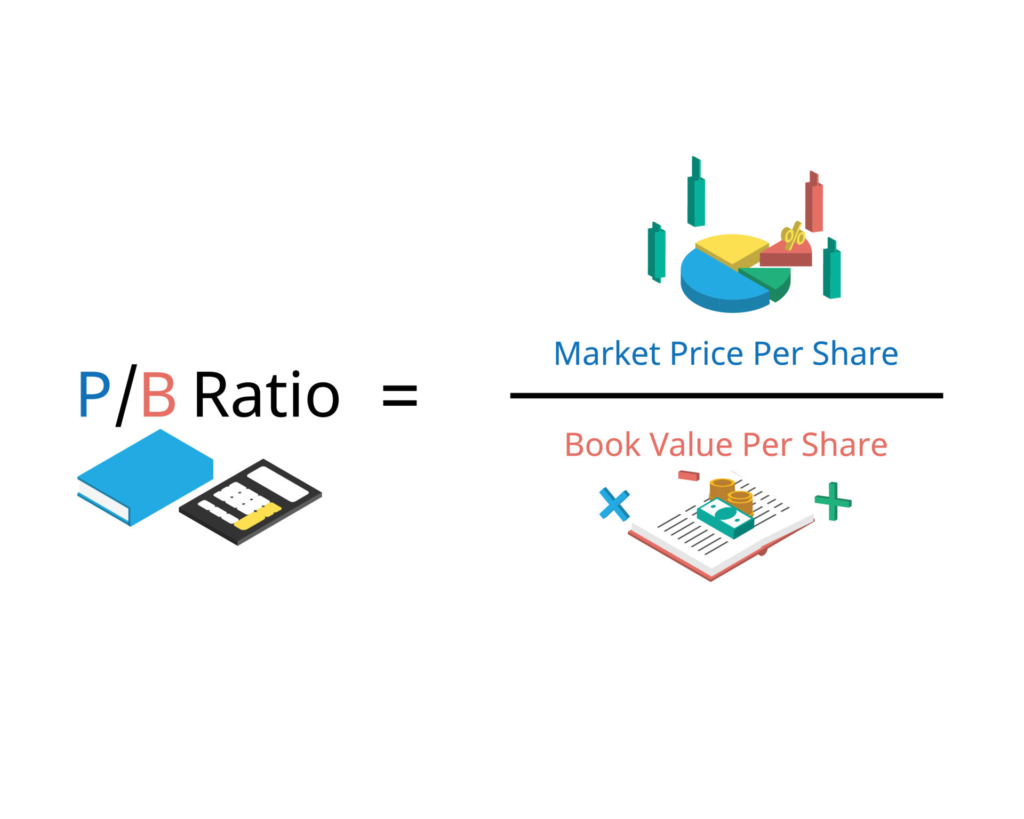

3. Price-to-Book (P/B) Ratio: This ratio compares a company’s market value to its book value, which is the value of the company’s assets minus its liabilities. A lower P/B ratio may indicate an undervalued stock.

- P/B Ratio: Calculated by dividing the market price per share by the book value per share.

- Interpretation: A P/B ratio below 1 may indicate undervaluation, while a ratio above 1 may suggest overvaluation.

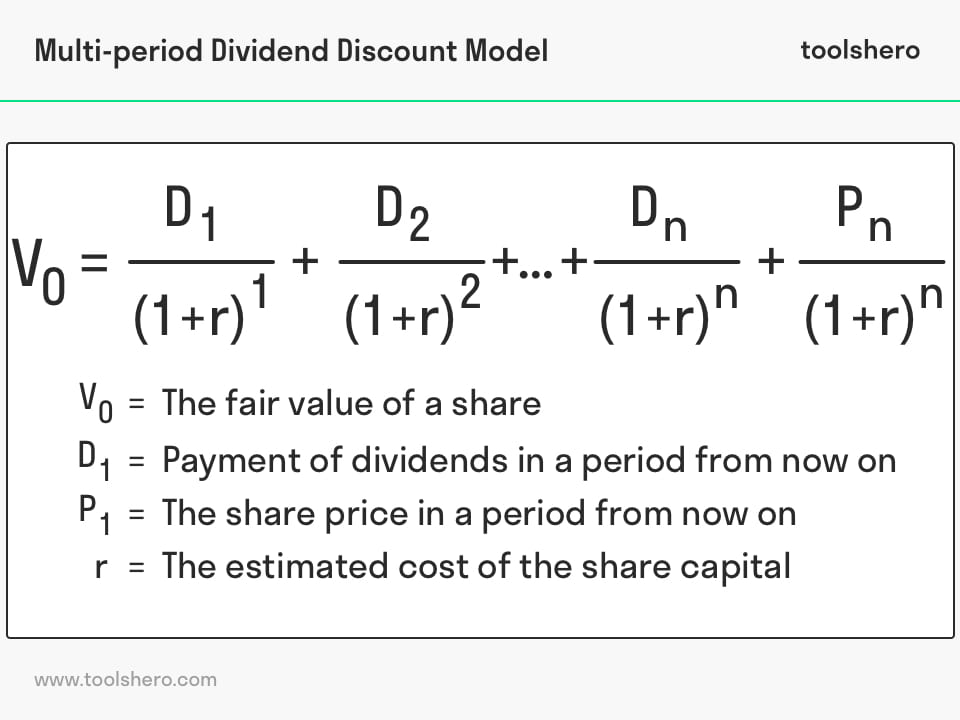

4. Dividend Discount Model (DDM): This method is used for companies that pay regular dividends. It calculates the present value of expected future dividends, assuming dividends will grow at a constant rate, for example, the Gordon Growth model.

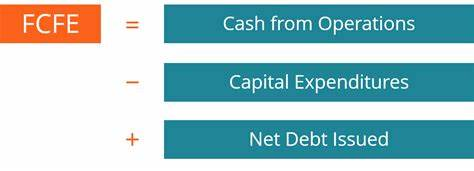

5. Free Cash Flow to Equity (FCFE): This approach focuses on the cash flows available to equity shareholders after accounting for operating expenses, capital expenditures, and debt payments. The present value of these cash flows gives the equity value.

- Calculate FCFE: Subtract capital expenditures and debt repayments from operating cash flows.

- Discount Rate: Use the cost of equity as the discount rate.

- Present Value: Discount the projected FCFE to present value and sum them up for the equity value.

6. Comparable Company Analysis (CCA): This method compares the company’s financial metrics (such as P/E ratio, P/B ratio, and EV/EBITDA) to those of similar companies in the same industry. It helps determine whether the stock is fairly priced compared to its peers.

- Select Comparables: Identify companies in the same industry with similar characteristics.

- Valuation Multiples: Use metrics like P/E, P/B, and EV/EBITDA to compare.

- Adjustments: Make adjustments for differences in size, growth rates, and profitability.

7. Sum of the Parts (SOTP): This method is used for conglomerates or companies with diverse business segments. Each segment is valued separately, and the total value is the sum of the individual segment values.

- Segment Valuation: Value each business segment separately using appropriate methods.

- Aggregate Value: Sum the individual segment values to get the total company value.

8. Economic Value Added (EVA): EVA measures a company’s financial performance based on the residual wealth created after deducting the cost of capital. It helps assess whether the company is generating value for its shareholders.

- Calculate EVA: Subtract the cost of capital from the net operating profit after taxes (NOPAT).

- Interpretation: Positive EVA indicates value creation, while negative EVA suggests value destruction.

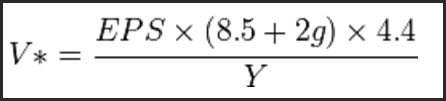

9. Graham’s Intrinsic Value: Graham’s intrinsic value formula is shown in the image below.

V: Intrinsic Value of the company,

EPS: the company’s last 12-month earnings per share,

8.5: the appropriate P-E ratio for a no-growth company as proposed by Graham,

g: the company’s long-term (five years) earnings growth estimate,

4.4: the average yield of high-grade corporate bonds,

Y: the current yield on 20-year AAA corporate bonds.

For a tech company like Apple, analysts might use DCF to project future cash flows from product sales and services.

A mature company with stable dividends, like Procter & Gamble, might be valued using the DDM.

For startups or high-growth companies, P/E and P/B ratios might be less relevant, and methods like FCFE and DCF would be more appropriate.

Each method has its strengths and weaknesses, and analysts often use a combination of these approaches to arrive at a more comprehensive valuation. Remember, the goal is to get an estimate of the stock’s intrinsic value to make informed investment decisions.

Real Estate valuation

Valuing real estate involves assessing various factors to determine the property’s market value. Here are some common methods used in real estate valuation:

- Comparable Sales Approach (Market Approach): This method compares the property with similar properties that have recently been sold in the same area. Adjustments are made for differences in features, size, condition, and location to estimate the property’s value.

- Identify Comparables: Find similar properties (comps) that have recently been sold in the same area.

- Adjustments: Make adjustments for differences in features, size, condition, location, and other factors to match the subject property.

- Market Trends: Consider current market conditions and trends to ensure an accurate estimate.

- Income Approach: This approach is primarily used for income-generating properties, like rental apartments or commercial buildings. It involves calculating the present value of future income streams the property is expected to generate. This can be done using the Gross Rent Multiplier (GRM) or Capitalization Rate (Cap Rate) methods.

- Net Operating Income (NOI): Calculate the NOI by subtracting operating expenses from gross rental income.

- Capitalization Rate (Cap Rate): Determine the Cap Rate based on market conditions and comparable properties.

- Valuation: Divide the NOI by the Cap Rate to estimate the property’s value.

- Cost Approach: This method estimates the value of the property by calculating the cost to replace or reproduce it, minus any depreciation. It involves adding the land value to the cost of constructing a similar property, accounting for factors like labor, materials, and building codes.

- Replacement Cost: Estimate the cost to replace or reproduce the property, including materials and labor.

- Depreciation: Subtract depreciation to account for wear and tear or obsolescence.

- Land Value: Add the value of the land to get the total property value.

- Sales Comparison Method: This method is similar to the Comparable Sales Approach but focuses more on specific characteristics and features that influence the property’s value, such as the number of bedrooms, square footage, amenities, and condition.

- Detailed Analysis: Examine specific characteristics and features that influence value, such as number of bedrooms, square footage, amenities, and condition.

- Market Data: Use recent sales data to provide a detailed and accurate comparison.

- Automated Valuation Models (AVMs): AVMs use algorithms and large databases of property information to estimate the value of real estate. These models consider factors like location, property size, recent sales, and market trends. Examples of AVMs include Zillow’s Zestimate and CoreLogic’s ValueMap.

- Data Analysis: Analyze factors like location, property size, recent sales, and market trends.

- Algorithm: Use statistical models to estimate property value quickly and efficiently.

- Examples: Zillow’s Zestimate, CoreLogic’s ValueMap.

- Highest and Best Use Analysis: This method involves analyzing the potential uses of the property to determine its highest and best use. This means considering the most profitable, legally permissible, physically possible, and financially feasible use of the property.

- Legally Permissible: Ensure the use complies with zoning laws and regulations.

- Physically Possible: Assess the feasibility of the use based on the property’s physical characteristics.

- Financially Feasible: Ensure the use provides a reasonable return on investment.

- Maximally Productive: Identify the use that maximizes the property’s value.

- Hedonic Pricing Model: This approach uses statistical analysis to estimate the value of a property based on its characteristics and attributes, such as location, size, number of rooms, and proximity to amenities. It helps understand how specific features impact the overall value.

- Characteristics: Analyze features like location, size, number of rooms, proximity to amenities, and condition.

- Regression Analysis: Use regression models to determine how each characteristic impacts value.

- Income Capitalization Approach: This approach is used for commercial properties and involves capitalizing the property’s net operating income (NOI). The value is calculated by dividing the NOI by the capitalization rate (Cap Rate), which reflects the investor’s required rate of return.

- NOI Calculation: Determine the property’s net operating income (NOI).

- Capitalization Rate: Use a Cap Rate to reflect the investor’s required rate of return.

- Valuation: Divide the NOI by the Cap Rate to estimate the property’s value.

Comparable Sales Approach by comparing recently sold similar properties in the neighborhood can be used for residential properties. Apply the Income Approach by calculating the NOI and using the Cap Rate to estimate the value of commercial properties. For commercial real estate the cost is based on the economic activity happening per unit area of the land.

Use the Cost Approach to estimate the cost of reproducing the property, including land value and depreciation for under-construction property.

Each method has its strengths and is used depending on the type of property and the purpose of the valuation. A thorough valuation often involves a combination of these approaches to provide a more accurate estimate of the property’s market value.

Rare Metal/ commodity valuation

Demand and supply.

Valuing precious metals, such as gold, silver, platinum, and palladium, involves several key factors and methods:

- Market Price: Precious metals are traded on global commodity markets, where their prices are determined by supply and demand dynamics. The most common way to check the value is to look at the spot price, which is the current market price for immediate delivery. This price fluctuates constantly based on market conditions.

- Weight and Purity: The value of a precious metal is often based on its weight and purity. The purity is usually expressed in terms of karats for gold (e.g., 24K gold is pure gold) or as a percentage or parts per thousand for other metals (e.g., 99.9% pure silver).

- Weight: Measured in troy ounces, grams, or kilograms.

- Purity: Often expressed in karats for gold (e.g., 24K is pure gold) or in percentage/parts per thousand for other metals (e.g., 99.9% pure silver).

- Futures Contracts: Futures contracts are agreements to buy or sell a specific amount of precious metal at a predetermined price on a specific date in the future. The prices of these contracts can influence the spot price of the metals.

- Exchange-Traded Funds (ETFs): ETFs track the price of precious metals and are traded on stock exchanges. The price of these ETFs reflects the market price of the underlying metal.

- Industrial and Jewelry Demand: The demand for precious metals in industries (such as electronics and automotive) and jewelry can significantly impact their value. High demand usually drives prices up.

- Economic Factors: Economic conditions, inflation, interest rates, and currency values can influence the prices of precious metals. For example, during economic uncertainty or inflation, investors often turn to precious metals as a safe haven, driving up their value.

- Geopolitical Events: Political instability, conflicts, and changes in government policies can affect the supply and demand of precious metals, influencing their prices.

- Central Bank Reserves: Central banks hold significant amounts of precious metals, especially gold, as part of their reserves. Their buying and selling activities can impact market prices.

- Mining Supply: The supply of precious metals from mining operations affects their availability and prices. Factors like mining production rates, exploration success, and geopolitical risks in mining regions can influence the supply side.

- Retail Premiums: When buying precious metals in physical forms, such as coins or bars, a retail premium is often added to the spot price. This premium covers manufacturing, distribution, and dealer costs.

Gold: Gold’s value is heavily influenced by investor sentiment, central bank policies, and economic conditions. It’s often seen as a safe haven during times of economic uncertainty.

Silver: Silver’s value is driven by industrial demand (e.g., electronics, solar panels) and its use in jewelry. It tends to be more volatile than gold due to its dual role as both an industrial and precious metal.

Platinum and Palladium: These metals are primarily used in the automotive industry for catalytic converters. Their prices are influenced by automotive demand, supply constraints, and geopolitical factors.

Valuing precious metals involves a combination of market analysis, understanding industrial and economic factors, and considering geopolitical events. Staying updated with market trends and economic indicators is essential for accurate valuation and informed decision-making.

Investors and analysts typically use a combination of these factors to value precious metals and make informed decisions. Additionally, staying updated with market trends and economic indicators is essential for accurate valuation.

This is all for this post, see you all in the next post. Don’t forget to follow my Facebook and Instagram pages for regular updates. Till then keep learning.