In the previous posts, we had discussed personal finances. If you have not seen those posts, you can check them out here. In this post, we are going to discuss leverage, more precisely, Loan vs Credit Line.

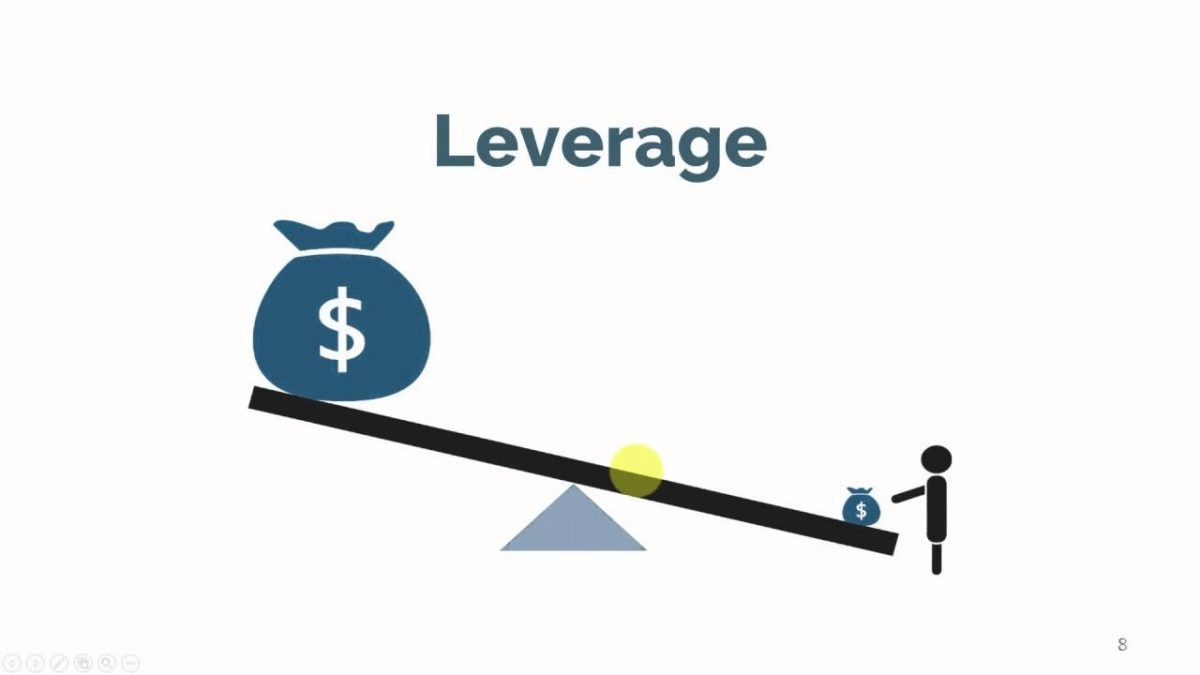

So first of all, what is Leverage?

The word “leverage” can be used in a few different ways depending on context, but it always has the sense of using something to gain an advantage. Leverage is like using a financial “lever” to lift more than you could with your strength alone. But if you overextend, the weight might come crashing down.

In finance, leverage refers to the strategy of using borrowed money to increase the potential return on investment. It’s a way to amplify gains—but also comes with the risk of magnifying losses if things don’t go as planned. This is useful for companies or investors who use debt as a tool to invest in assets or projects. The idea here is that the return from investment will be greater than the cost of borrowing. Leverage ratio is a common measure of financial leverage. It compares debt to equity (or assets). A high ratio means more debt is being used.

Ways to borrow money

So what are the ways to borrow Money or use leverage? There are two common ways to borrow money.

Loan

The first way to borrow money is to take a loan. So what’s a loan?

A loan gives you a lump sum of money upfront, which you repay over time in fixed installments known as EMIs (Equated Monthly Installments). The interest on the full amount starts accruing immediately. This is mostly used to fund big-ticket expenses like buying a car, a home, or funding education.

Credit Line

A credit line (or line of credit) is a flexible borrowing option that lets you access funds as needed, up to a set limit. A credit line has the concept of revolving credit, that is, you can borrow, repay, and borrow again. Unlike a loan, the interest is not charged on the complete disbursed amount but on the used amount. This has a flexible repayment option, which allows you can make a minimum payment or full balance repayment. This is best for ongoing or predictable expenses like renovations, emergencies, or business cash flow.

Below is a summary of Loan vs Credit Line.

| Feature | Loan | Credit Line |

| Disbursement | Lump sum | As needed, up to credit limit |

| Repayment | Fixed EMIs | Flexible, based on usage |

| Interest | Only on the borrowed amount | Only on borrowed amount |

| Use Case | One-time large expenses | Ongoing or variable expenses |

| Flexibility | Low | High |

| Interest Rate | Usually lower (fixed) | Often higher (variable) |

Types of Loan

Now, under loans also there are two types of loans. Read ahead to find out.

Secured Loan

These require collateral—an asset the lender can claim if you default.

- Home Loan: For purchasing or constructing a property. The house itself is the collateral.

- Loan Against Property: Borrow against residential or commercial property.

- Gold Loan: Pledge gold jewelry for quick funds.

- Vehicle Loan: Finance for cars, bikes, or commercial vehicles.

- Loan Against Fixed Deposit: Borrow against your FD without breaking it.

- Loan Against Securities: Use shares, mutual funds, or bonds as collateral.

- Loan Against Insurance Policy: Available if the policy has a surrender value.

This collateral is seized if the borrower defaults, that is, the borrower fails to repay the amount borrowed with interest.

Unsecured Loans

No collateral needed—approval depends on your creditworthiness.

- Personal Loan: Versatile use—medical, travel, wedding, etc.

- Education Loan: For higher studies in India or abroad.

- Credit Card Loan: Pre-approved loans based on your card limit.

- Business Loan: For entrepreneurs and SMEs to fund operations or expansion.

- Payday Loan: Short-term loan until your next salary—often with high interest.

- Flexi Loan: Withdraw funds as needed from a pre-approved limit.

Since there is no collateral, there is nothing that the lender can seize. Thus, this type of loan carries a higher interest rate as compared to a secured loan, as the risk is higher.

Specialized Loans

This type of loan is tailored for specific groups or purposes.

- Agriculture Loan: For farmers to buy equipment or fund crop production.

- Mudra Loan: Government-backed loans for small businesses.

- Home Renovation Loan: For upgrading or repairing your home.

- Consumer Durable Loan: Finance for electronics or appliances.

- Travel Loan: Covers vacation expenses.

- Medical Loan: For planned or emergency healthcare costs.

Here is a summary of loans that require collateral or don’t, and their common use cases.

| Loan Type | Collateral Required | Common Use Case |

| Home Loan | Yes | Buying property |

| Personal Loan | No | General expenses |

| Education Loan | No | Higher studies |

| Gold Loan | Yes (Gold) | Emergency funds |

| Business Loan | Depends | Business needs |

| Vehicle Loan | Yes (Vehicle) | Buying a car/bike |

| Loan Against FD | Yes (FD) | Liquidity without breaking FD |

So, which should you use for borrowing, a loan or a credit line? Read ahead to get a clearer picture to understand the advantages and disadvantages of both.

Credit Line

Advantages of a Credit Line

- Flexible Access to Funds – Borrow only what you need, when you need it—great for unpredictable expenses or emergencies.

- Interest on Used Amount Only – Unlike loans, you pay interest only on the amount you borrow, not the full credit limit.

- Revolving Credit – Repay and reuse the funds repeatedly without reapplying, as long as you stay within the limit.

- Lower Interest Rates (Compared to Credit Cards) – Especially for secured credit lines, rates are often more favorable than traditional credit cards.

- Improves Credit Score – Responsible use and timely repayments can boost your credit profile over time.

- Quick Access to Cash – Funds are typically available faster than traditional loans—sometimes within 24 hours.

Disadvantages of a Credit Line

- Temptation to Overspend – Easy access can lead to unnecessary borrowing and debt accumulation.

- Variable Interest Rates – Most credit lines have adjustable rates, which can rise unexpectedly and increase your repayment burden.

- Fees and Penalties – Annual fees, transaction charges, and penalties for late payments or inactivity can add up.

- No Grace Period – Interest starts accruing immediately upon withdrawal—unlike credit cards that offer a grace period.

- Qualification Requirements – You’ll need a good credit score, stable income, and sometimes collateral to qualify.

- Limited Regulation – Credit lines may be less regulated than credit cards, so terms and protections vary widely.

Loan

Advantages of a Loan

- Access to Large Funds – Loans allow you to make big purchases (like a home or car) or investments without needing the full amount up front.

- Structured Repayment – Fixed EMIs (Equated Monthly Installments) make budgeting easier and help you plan your finances.

- Lower Interest Rates (for Secured Loans) – Compared to credit cards or payday loans, secured loans often come with more favorable rates.

- Tax Benefits – Interest paid on certain loans (like home loans or education loans) may be tax-deductible.

- Builds Credit History – Timely repayments can improve your credit score and make future borrowing easier.

- Ownership Retention – Unlike equity financing, loans don’t require giving up ownership in your business or assets.

Disadvantages of a Loan

- Repayment Pressure – Monthly payments are mandatory—missing them can lead to penalties or damage your credit score.

- Interest Costs – You’ll pay more than you borrow due to interest, especially with long-term or high-rate loans.

- Collateral Risk (for Secured Loans) – If you default, the lender can seize your asset (home, car, etc.).

- Strict Eligibility Criteria – Banks often require good credit scores, stable income, and documentation—making approval tough for some.

- Hidden Fees – Origination charges, processing fees, and prepayment penalties can add to the cost.

- Impact on Future Borrowing – A high debt-to-income ratio may limit your ability to take on new loans.

So which one should you choose?

Choose a loan if you need a large, one-time amount with predictable payments. Opt for a credit line if you want flexibility and access to funds over time.

Leverage might cost you interest, but open doors that otherwise might have been missed due to the lack of funds, also known as opportunity cost.

This is all for this post, hope you got to learn something new from this post. Don’t forget to follow my Facebook and Instagram pages for regular updates. See you all in the next post, till then keep learning.